Futures Market: Overnight, LME copper opened at $9,754.5/mt, initially fluctuating upward to a high of $9,809.5/mt before fluctuating downward. It approached the session low at $9,702.5/mt near the close and eventually settled at $9,707.5/mt, up 0.61%. Trading volume reached 28,000 lots, and open interest reached 283,000 lots. Overnight, the most-traded SHFE copper 2507 contract opened at 78,960 yuan/mt, initially rising to a high of 79,180 yuan/mt before fluctuating downward throughout the session. It approached the session low at 78,490 yuan/mt near the close and eventually settled at 78,570 yuan/mt, up 0.58%. Trading volume reached 75,000 lots, and open interest reached 199,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) Data released by Chilean Customs showed that Chile's copper exports in May totaled 181,234 mt, with 32,721 mt exported to China in the same month. Copper ore and concentrate exports from Chile in May reached 1,485,670 mt, with 978,141 mt exported to China. Chile's copper production has rebounded in the past two months, and copper and copper ore exports to China have also significantly recovered from over a year's low.

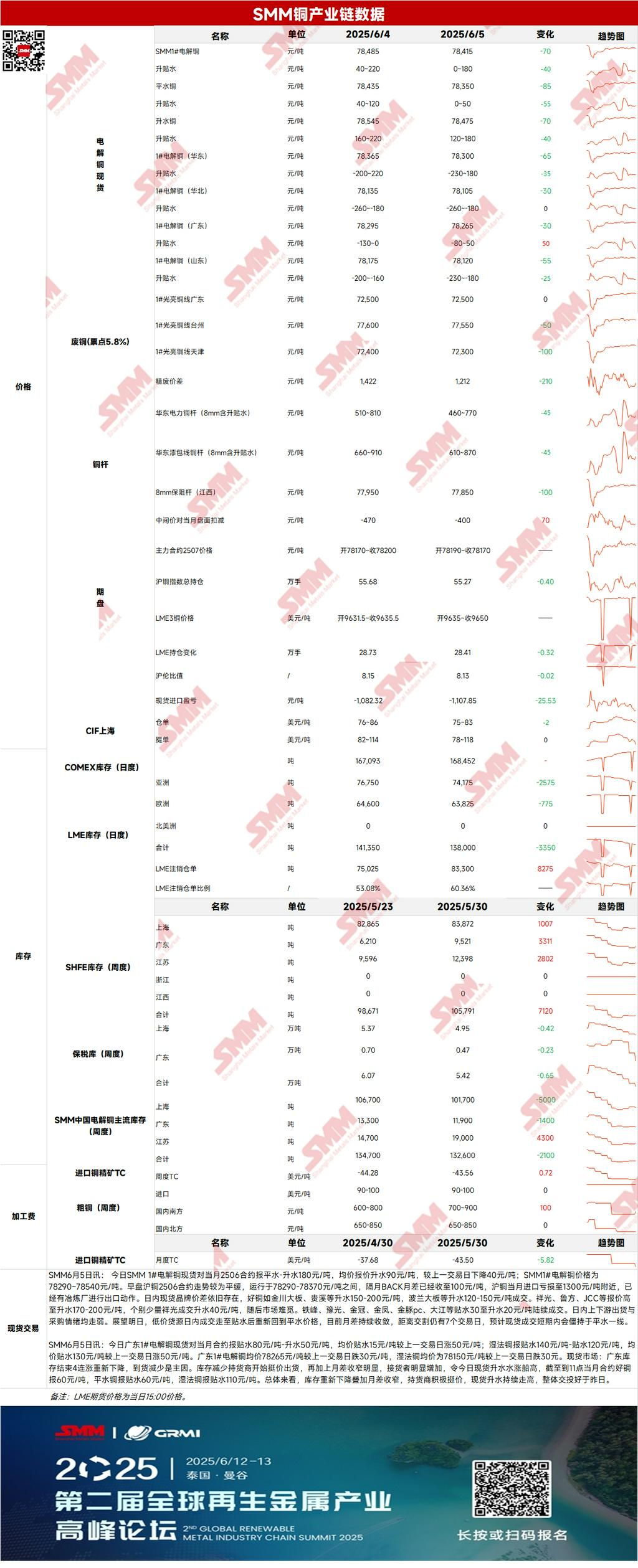

Spot: (1) Shanghai: On June 5, SMM #1 copper cathode spot prices against the front-month 2506 contract were quoted at parity to a premium of 180 yuan/mt, with an average premium of 90 yuan/mt, down 40 yuan/mt from the previous trading day. The SMM #1 copper cathode price range was 78,290-78,540 yuan/mt. In the morning session, the SHFE copper 2506 contract traded relatively flat within the range of 78,290-78,370 yuan/mt. The backwardation between the front-month and next-month contracts had narrowed to 100 yuan/mt, and the import loss for front-month SHFE copper was around 1,300 yuan/mt, prompting some smelters to initiate exports. Looking ahead to tomorrow, after low-priced cargoes were traded at a discount earlier in the day, prices have returned to parity. With the continuous narrowing of the price spread between futures contracts and seven trading days remaining until delivery, spot transactions are expected to remain stagnant around parity in the short term.

(2) Guangdong: On June 5, Guangdong's #1 copper cathode spot prices against the front-month contract were quoted at a discount of 80 yuan/mt to a premium of 50 yuan/mt, with an average discount of 15 yuan/mt, up 50 yuan/mt from the previous trading day. SX-EW copper was quoted at a discount of 140 yuan/mt to a discount of 120 yuan/mt, with an average discount of 130 yuan/mt, up 50 yuan/mt from the previous trading day. The average price of Guangdong's #1 copper cathode was 78,265 yuan/mt, down 30 yuan/mt from the previous trading day, while the average price of SX-EW copper was 78,150 yuan/mt, also down 30 yuan/mt from the previous trading day. Overall, with inventory declining again and the price spread between futures contracts narrowing, suppliers are actively refusing to budge on prices, leading to a continuous rise in spot premiums. Overall trading activity was better than yesterday.

(3) Imported Copper: On June 5, warrant prices ranged from $75 to $83/mt, with a QP of June, and the average price fell by $2/mt from the previous trading day. B/L prices ranged from $82 to $114/mt, with a QP of July, and the average price remained unchanged from the previous trading day. EQ copper (CIF B/L) prices ranged from $38 to $54/mt, with a QP of July, and the average price remained unchanged from the previous trading day. Quotations were based on cargoes expected to arrive in mid-to-late June. The market was relatively sluggish during the day, with buyers still offering low prices and few offers from sellers. Both buyers and sellers were inactive. Inventories in bonded zones stopped falling and rebounded during the week, while warrant prices continued to decline.

(4) Secondary copper: On June 5, the price of secondary copper raw materials rose by 200 yuan/mt MoM. The price of bare bright copper in Guangdong was 72,400-72,600 yuan/mt, up 200 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,422 yuan/mt, rising by 87 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,130 yuan/mt. According to the SMM survey, as various regions gradually strengthen the enforcement of "reverse invoicing," some secondary copper rod enterprises have reported that local tax authorities have suspended issuing VAT invoices for small and micro enterprises. As provinces and cities continue to advance this policy, the input tax credits for secondary copper rod enterprises will be dominated by "reverse invoicing" in the future.

(5) Inventory: On June 5, LME copper cathode inventory decreased by 3,350 mt to 138,000 mt. On the same day, SHFE warrant inventory fell by 246 mt to 31,687 mt.

Prices: On the macro front, US data showed that initial jobless claims surged to an 8-month high last week. Amidst escalating economic headwinds from tariffs, the labour market conditions softened, putting pressure on the US dollar and supporting copper prices. The market is now awaiting guidance from the non-farm payrolls report on Friday. On the fundamental front, there were significant differences in the premiums of various brands of copper cathode during the day, with large fluctuations in premiums. Demand side, both upstream shipments and downstream procurement sentiment weakened, with sluggish downstream consumption and a clear willingness to negotiate prices. As of Thursday, June 5, SMM's national copper inventories in major regions decreased by 4,000 mt from Monday to 149,000 mt, up 10,000 mt from last Thursday, an increase of 29,000 mt from the recent low, and 302,000 mt lower than the 451,000 mt recorded in the same period last year. In terms of prices, it is expected that there will be limited upside potential for today's prices.

[The information provided is for reference only. This article does not constitute direct advice for investment research and decision-making. Clients should make prudent decisions and should not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]